Home Credit: A Comprehensive Guide to Financing Your Dream Home

Related Articles: Home Credit: A Comprehensive Guide to Financing Your Dream Home

Introduction

With great pleasure, we will explore the intriguing topic related to Home Credit: A Comprehensive Guide to Financing Your Dream Home. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Home Credit: A Comprehensive Guide to Financing Your Dream Home

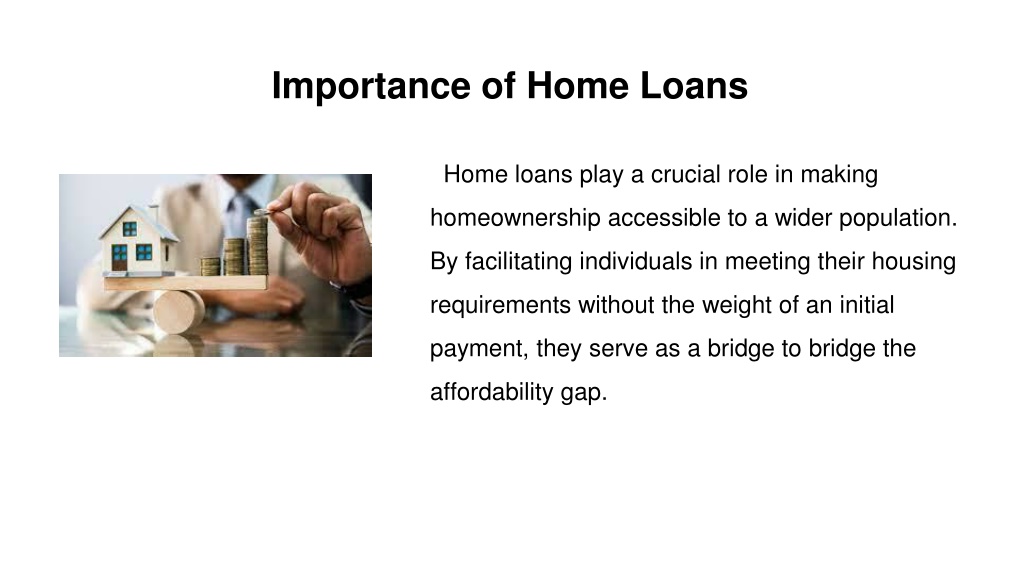

The dream of owning a home is a universal aspiration. It signifies stability, security, and a place to build cherished memories. However, the financial burden associated with purchasing a home can be daunting. This is where home credit, a specialized form of financing, comes into play.

Home credit, often referred to as a mortgage, allows individuals to borrow a significant sum of money to purchase a property, with the borrower making regular repayments over a predetermined period. This financial instrument plays a pivotal role in enabling individuals to achieve their homeownership goals, unlocking a world of possibilities and benefits.

Understanding the Mechanics of Home Credit

Home credit is a complex financial arrangement with various components that need to be understood to make informed decisions.

1. Loan Amount: This represents the total sum of money borrowed to purchase the property. The loan amount is typically determined by factors such as the property’s value, the borrower’s financial standing, and the lender’s lending policies.

2. Interest Rate: This is the cost of borrowing money, expressed as a percentage of the loan amount. The interest rate can fluctuate based on market conditions, the borrower’s creditworthiness, and the loan’s term.

3. Loan Term: This refers to the duration of the loan, typically ranging from 15 to 30 years. The loan term influences the monthly repayment amount, with longer terms resulting in lower monthly payments but higher overall interest costs.

4. Down Payment: This is the initial amount of money paid towards the property’s purchase price. A larger down payment generally results in a smaller loan amount, leading to lower interest costs and monthly payments.

5. Mortgage Insurance: This is an insurance policy that protects the lender against potential losses in case of default by the borrower. The requirement for mortgage insurance varies based on the loan-to-value ratio (LTV), which is the ratio of the loan amount to the property’s value.

6. Closing Costs: These are expenses incurred during the home purchase process, including fees for legal services, appraisal, and title insurance.

Types of Home Credit

There are several types of home credit available, each tailored to different financial situations and borrower preferences:

1. Conventional Loans: These are the most common type of home credit, offered by private lenders and typically require a down payment of 20% or more. They offer competitive interest rates and flexible terms.

2. FHA Loans: Backed by the Federal Housing Administration (FHA), these loans are designed to make homeownership accessible to individuals with lower credit scores and down payments. They typically require a down payment of 3.5% or less.

3. VA Loans: Guaranteed by the Department of Veterans Affairs (VA), these loans are available to eligible veterans, active-duty military personnel, and surviving spouses. They offer no down payment requirement and competitive interest rates.

4. USDA Loans: Provided by the United States Department of Agriculture (USDA), these loans are designed to support rural development and homeownership in eligible areas. They offer low-interest rates and flexible terms, sometimes with no down payment requirement.

5. Jumbo Loans: These loans exceed the conforming loan limits set by Fannie Mae and Freddie Mac, catering to high-value properties. They often require higher credit scores and larger down payments.

Benefits of Home Credit

Home credit offers numerous advantages, making it a valuable financial tool for achieving homeownership:

1. Affordable Homeownership: By spreading the cost of the property over a long period, home credit makes homeownership accessible to individuals who may not have the financial resources to purchase outright.

2. Building Equity: With each monthly payment, borrowers build equity in their property, gradually increasing their ownership stake.

3. Tax Deductions: Interest paid on home loans is often tax-deductible, potentially reducing the borrower’s tax liability.

4. Stable Housing: Owning a home provides a sense of stability and security, offering protection from rising rental costs and market fluctuations.

5. Investment Opportunity: Real estate is often considered a sound investment, with the potential for appreciation over time.

Choosing the Right Home Credit Option

Selecting the appropriate home credit option is crucial for financial success. Several factors should be considered:

1. Credit Score: A higher credit score generally leads to lower interest rates and better loan terms.

2. Down Payment: A larger down payment can reduce the loan amount, resulting in lower monthly payments and interest costs.

3. Loan Term: The chosen loan term influences the monthly payment amount and total interest paid over the loan’s life.

4. Interest Rate: Comparing interest rates from different lenders is essential to secure the best deal.

5. Loan Fees and Closing Costs: Understanding the associated fees and costs is vital for budgeting purposes.

6. Financial Situation: Evaluating personal income, debt levels, and savings is crucial for determining affordability.

7. Future Plans: Considering future financial goals and potential changes in income or living situation can influence loan choices.

Frequently Asked Questions (FAQs) About Home Credit

1. What is the minimum credit score required for a home loan?

The minimum credit score requirement varies depending on the lender and loan type. However, a score of 620 or higher is generally considered favorable for most conventional loans.

2. How much can I borrow for a home loan?

The loan amount is typically based on your income, debt-to-income ratio (DTI), and the property’s value. Lenders often use a debt-to-income ratio of 43% as a guideline.

3. What are the different types of mortgage interest rates?

Common types of mortgage interest rates include fixed-rate mortgages, where the interest rate remains constant throughout the loan term, and adjustable-rate mortgages (ARMs), where the interest rate can fluctuate based on market conditions.

4. What are the benefits of a fixed-rate mortgage?

A fixed-rate mortgage provides predictable monthly payments and protection against rising interest rates.

5. What are the benefits of an adjustable-rate mortgage?

ARMs can offer lower initial interest rates compared to fixed-rate mortgages, making them attractive for borrowers who anticipate a short-term ownership period.

6. How do I apply for a home loan?

You can apply for a home loan through banks, credit unions, mortgage brokers, or online lenders.

7. What documents do I need to apply for a home loan?

Typically, you will need to provide documents such as your social security number, proof of income, bank statements, and credit report.

8. How long does it take to get approved for a home loan?

The approval process can take several weeks, depending on the lender and the complexity of your application.

9. What happens if I default on my home loan?

Defaulting on a home loan can result in foreclosure, where the lender can seize the property to recover the outstanding debt.

10. What are some tips for getting approved for a home loan?

Tips for Obtaining Home Credit

1. Improve Your Credit Score: A strong credit score is essential for securing favorable loan terms. Pay bills on time, manage debt levels, and avoid opening new credit accounts unnecessarily.

2. Save for a Down Payment: Aim for a down payment of at least 20% to avoid private mortgage insurance (PMI) and qualify for better loan options.

3. Get Pre-Approved for a Loan: Pre-approval from a lender demonstrates your financial readiness and strengthens your negotiating position when making offers on properties.

4. Shop Around for Interest Rates: Compare interest rates and loan terms from different lenders to find the best deal.

5. Understand Loan Fees and Costs: Be aware of all associated fees and costs, including closing costs, origination fees, and appraisal fees.

6. Get a Home Inspection: A thorough home inspection can identify potential problems and help you negotiate repairs with the seller.

7. Budget for Unexpected Expenses: Plan for unexpected expenses that may arise during the home purchase process, such as repairs or unforeseen costs.

8. Seek Professional Guidance: Consult with a financial advisor or mortgage broker to navigate the complex process and make informed decisions.

Conclusion

Home credit is a powerful financial tool that can unlock the door to homeownership. By understanding the mechanics, benefits, and different types of home credit, individuals can make informed decisions and achieve their dream of owning a home. Remember to thoroughly research, compare options, and seek professional guidance to ensure financial success on this exciting journey.

Closure

Thus, we hope this article has provided valuable insights into Home Credit: A Comprehensive Guide to Financing Your Dream Home. We hope you find this article informative and beneficial. See you in our next article!